Working Papers

The Effect of Firm Subsidies on Credit Markets

› abstract

Governments use firm subsidies to spark corporate investment, which may have repercussions in credit markets though. To test for potential credit market distortions due to this economic policy, we combine project-level information for the largest regional economic development program in German history with bank lending and firm borrowing over a long horizon: 1998–2019. Firm subsidies associate with larger lending volumes provided by banks. On the flip-side of credit markets, we document increased corporate borrowing. Importantly, we find neither evidence of excessively risky lending by banks nor crowding-out of credit to nonsubsidized firms. Firm subsidies support lending especially when credit constraints are elevated during the financial crisis. Overall, firm subsidies unfolded a positive multiplier effect in regional credit markets in our setting.

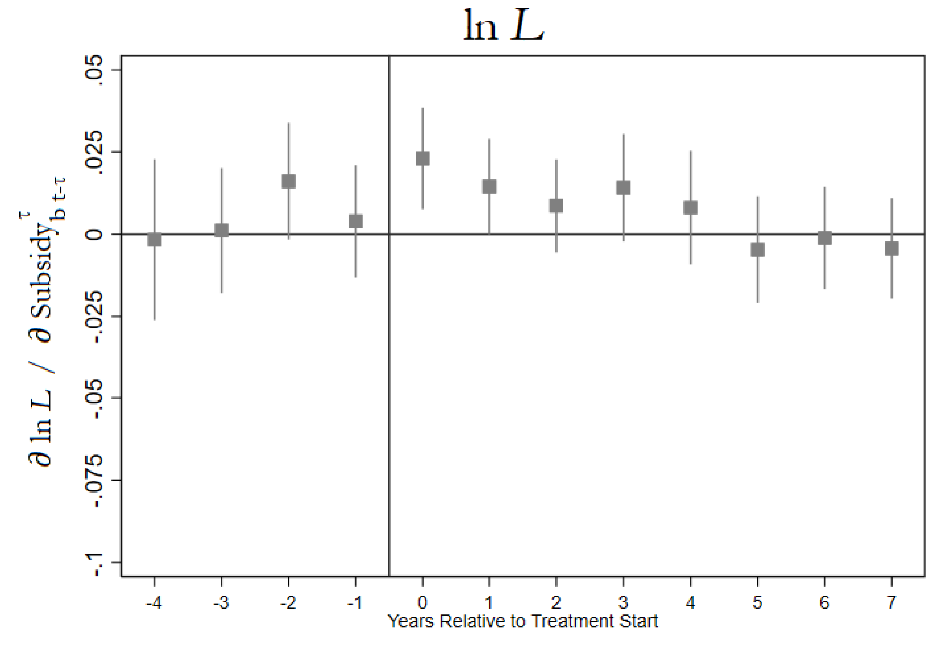

Figure 1. The figure shows the effect of the variable \( \text{Subsidy}_{b t-\tau}^{\tau} \) over time on the log-level of loans \( \ln L \) - the results from estimating the regression from Equation (6) of the paper:

\( Y_{it} = \alpha_i + \gamma_t + \beta X_{it} + \varepsilon_{it} \)

and plots the coefficient estimates for the \( \hat{\beta}_{1}^{\tau} \) coefficients and the 95% confidence bands. Subsidy exposure is based on links to subsidized firms in the first year of the subsidized project. The sample includes German savings and cooperative banks and spans the period from 1998 to 2019. Further controls include bank-level variables and averaged firm-level variables lagged by one period as those in Columns 1–5 of Table 5 of the paper. Bank and state-time fixed effects are included. See Table 2 of the paper for a detailed description of all variables.

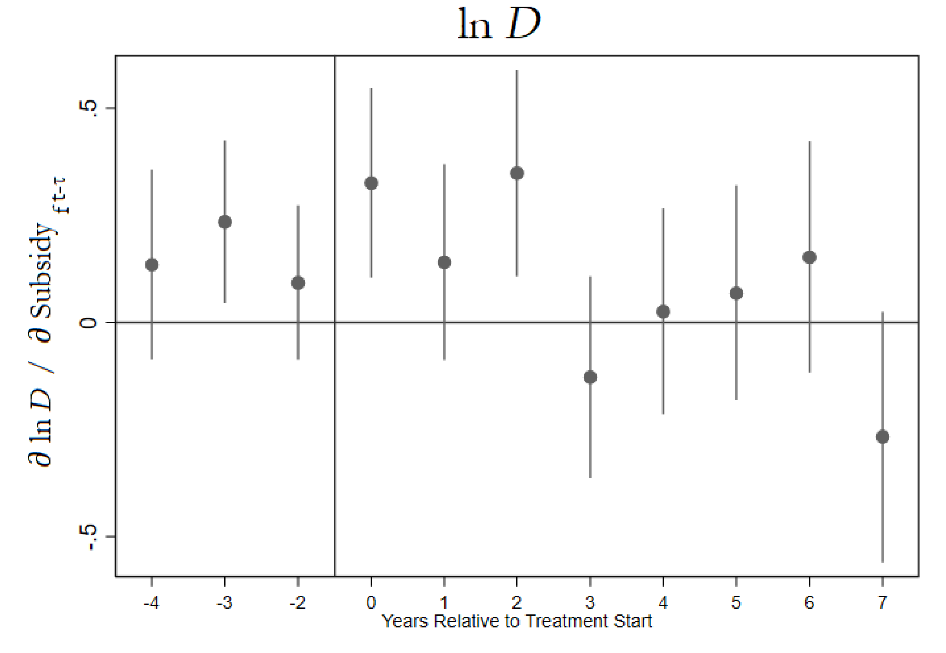

Figure 2. The figure shows the effect of the variable \( \text{Subsidy}_{f t-\tau} \) on the log-level of firms’ bank debt \( \ln D \) - the results from estimating the regression from Equation (7) of the paper:

\( Y_{it} = \alpha_i + \gamma_t + \beta X_{it} + \varepsilon_{it} \)

and plots the coefficient estimates for the \( \hat{\gamma}_{1}^{\tau} \) coefficients and the 95% confidence bands. The firm sample includes German firms and spans the period from 2002 to 2020 including a treatment group of subsidized firms and a control group of firms of the same 3-digit NACE industry matched using the coarsened exact matching approach based on the values of firms’ assets, cash ratio, capitalization, and fixed assets growth (%) as of one year before the firm received the subsidy. Further controls include firm-level variables lagged by one period. Firm and time fixed effects are included and standard errors are clustered at the firm level. See Table 2 of the paper for a detailed description of all variables.

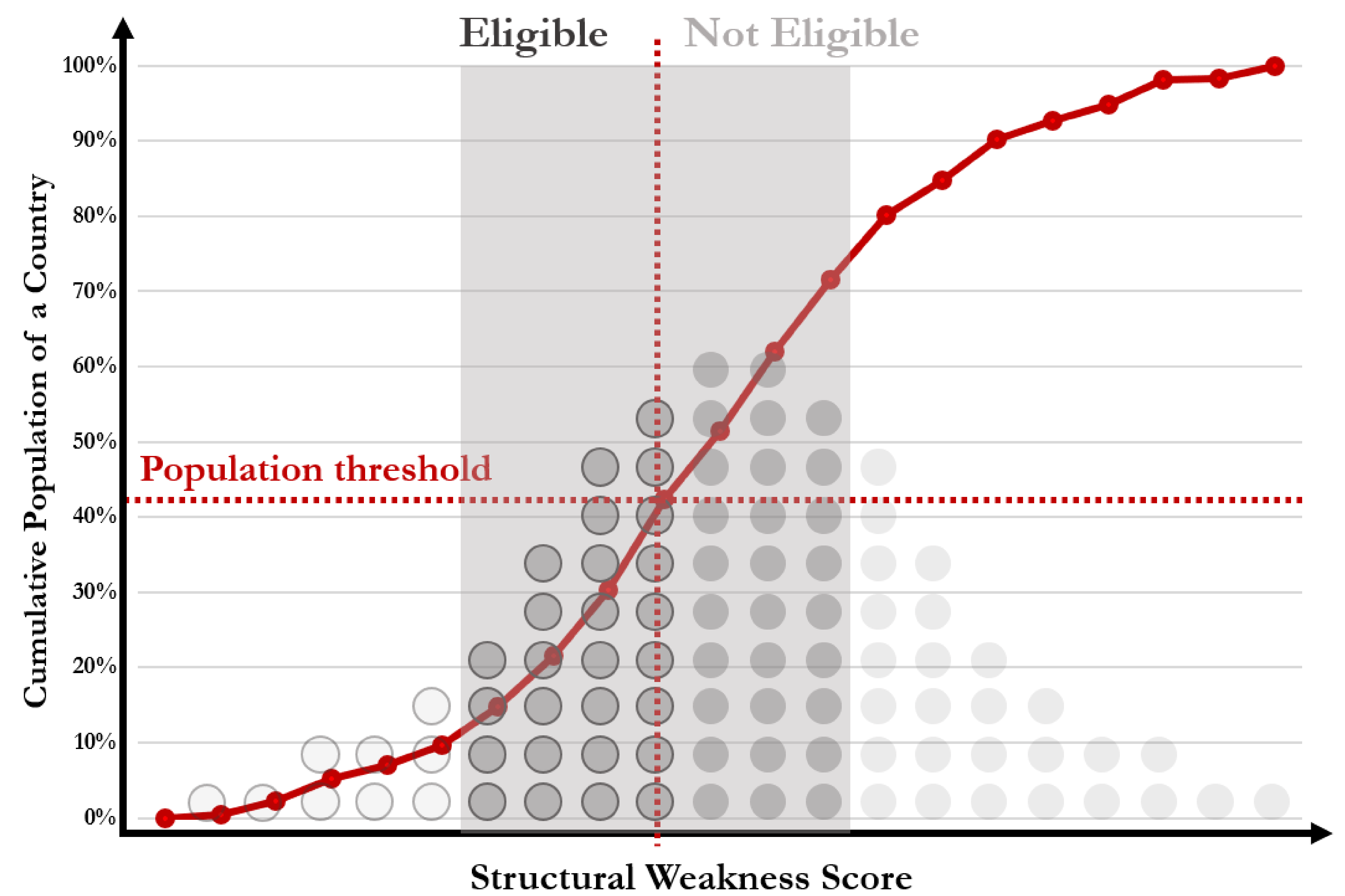

Figure 3. The figure illustrates the two key factors driving whether regions are eligible for the subsidy program. The x-axis depicts the structural weakness score assigned to labor market regions, the lower it is, the weaker is the region. The y-axis depicts the cumulative population share in a country’s total population. For Germany, this score is close to 40% across all years. All regions in the left part are eligible due to a low weakness score and because the population threshold has not yet been hit.

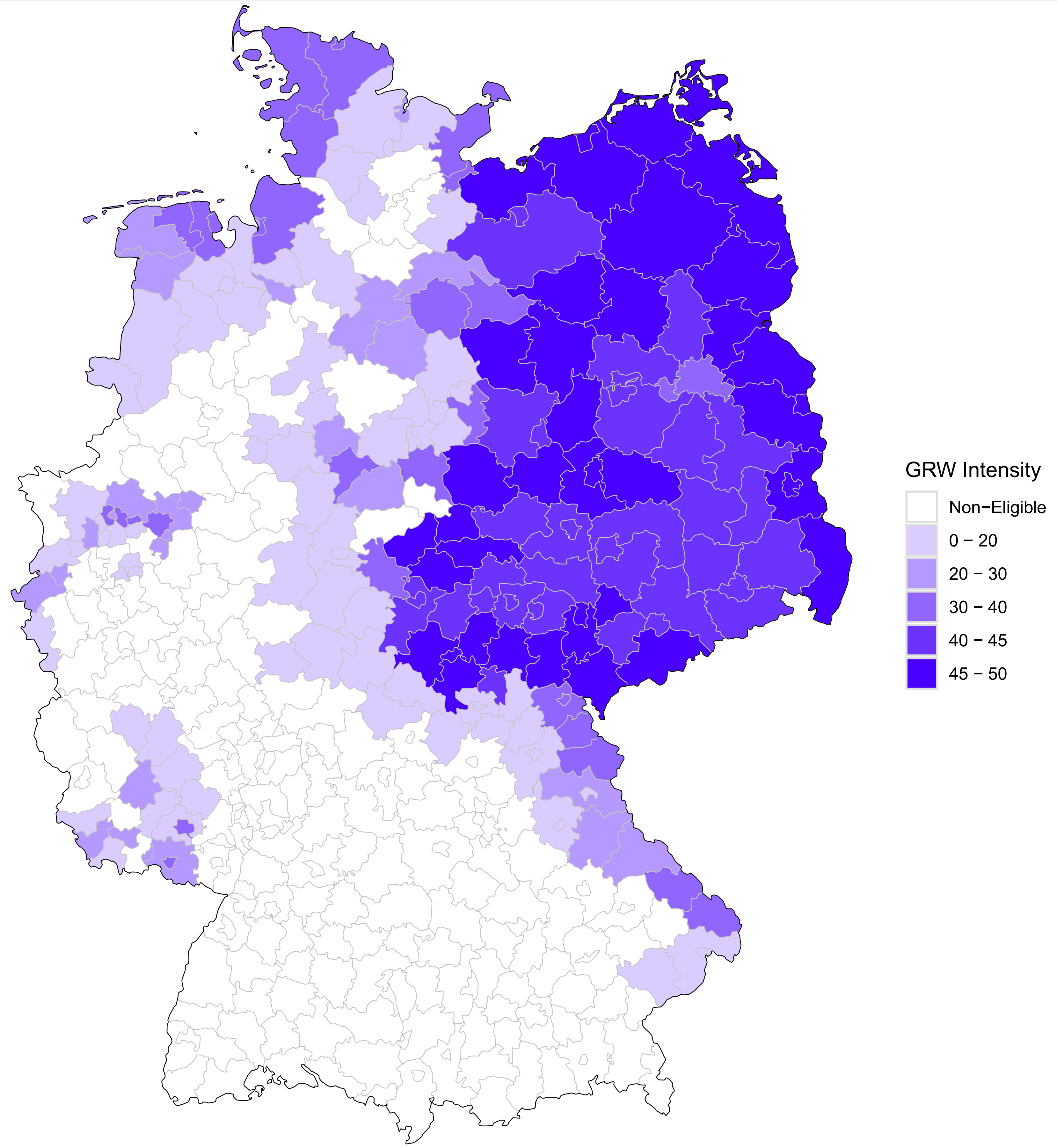

Figure 4. The figure illustrates the spatial distribution of aid intensities of the GRW program across Germany. Values for each county are calculated based on the average GRW intensity over the three last GRW program periods (2000-2019). Aid intensity is measured as the maximum share of the investment costs of a subsidized project, which can be covered by the subsidy

Quo Vadis? Bank Closures, Firm Performance, and New Bank-Firm Relationships

› abstract

Abstract: How do firms respond to sudden and forcible closures of their lenders? Using unique credit register data from a setting where two-thirds of banks were closed within a decade, we find that neither bad nor good firms delay repayments or switch lenders before closures. Afterward, bad firms lose subsidized credit and experience sharp declines in employment, borrowing, and sales, while good firms improve performance. This divergence stems from banks’ prior underpricing of bad firms’ credit risk. Ultimately, good firms match with new solid banks, while bad firms gravitate toward not-yet-detected weak banks—especially where boards overlap or markets are unconcentrated.

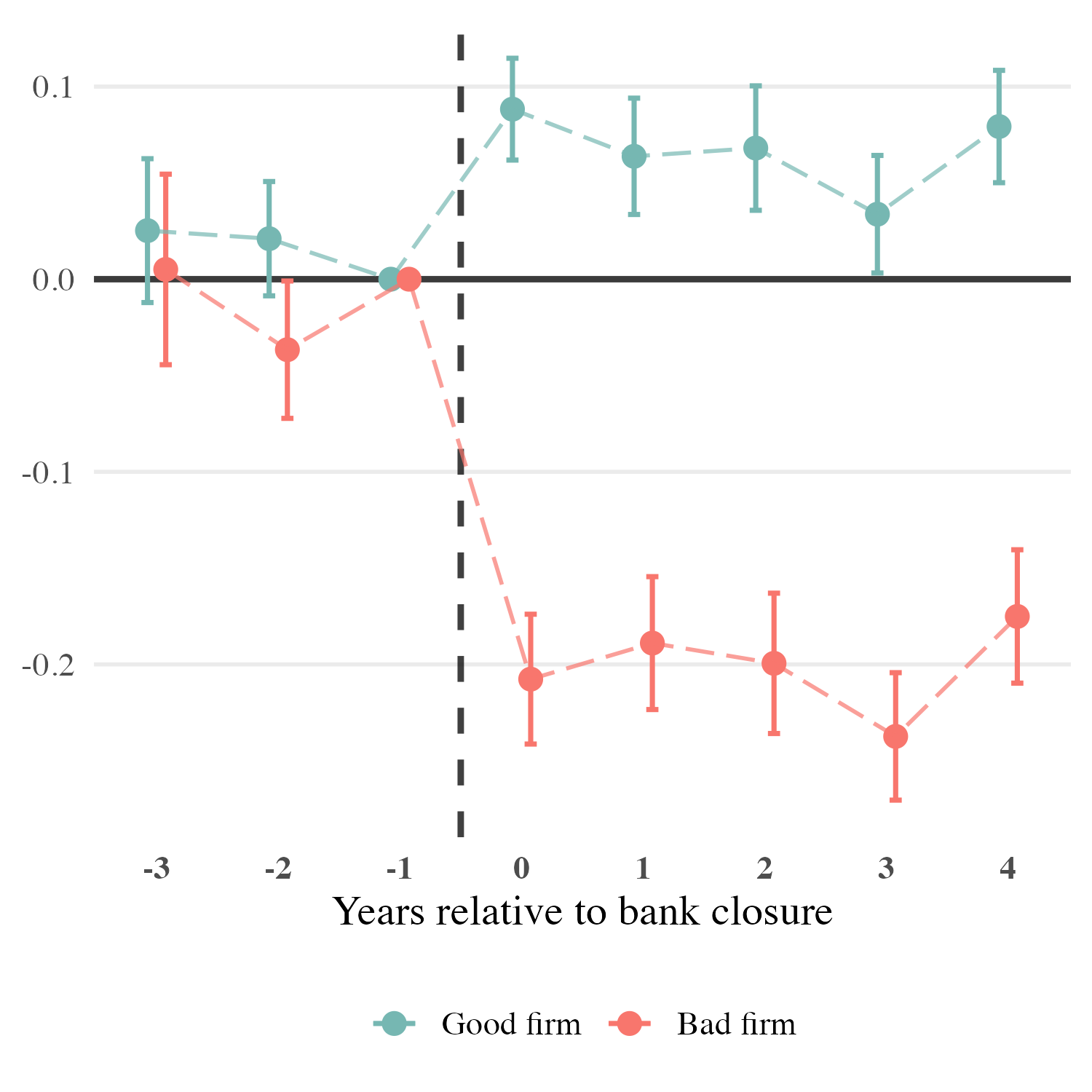

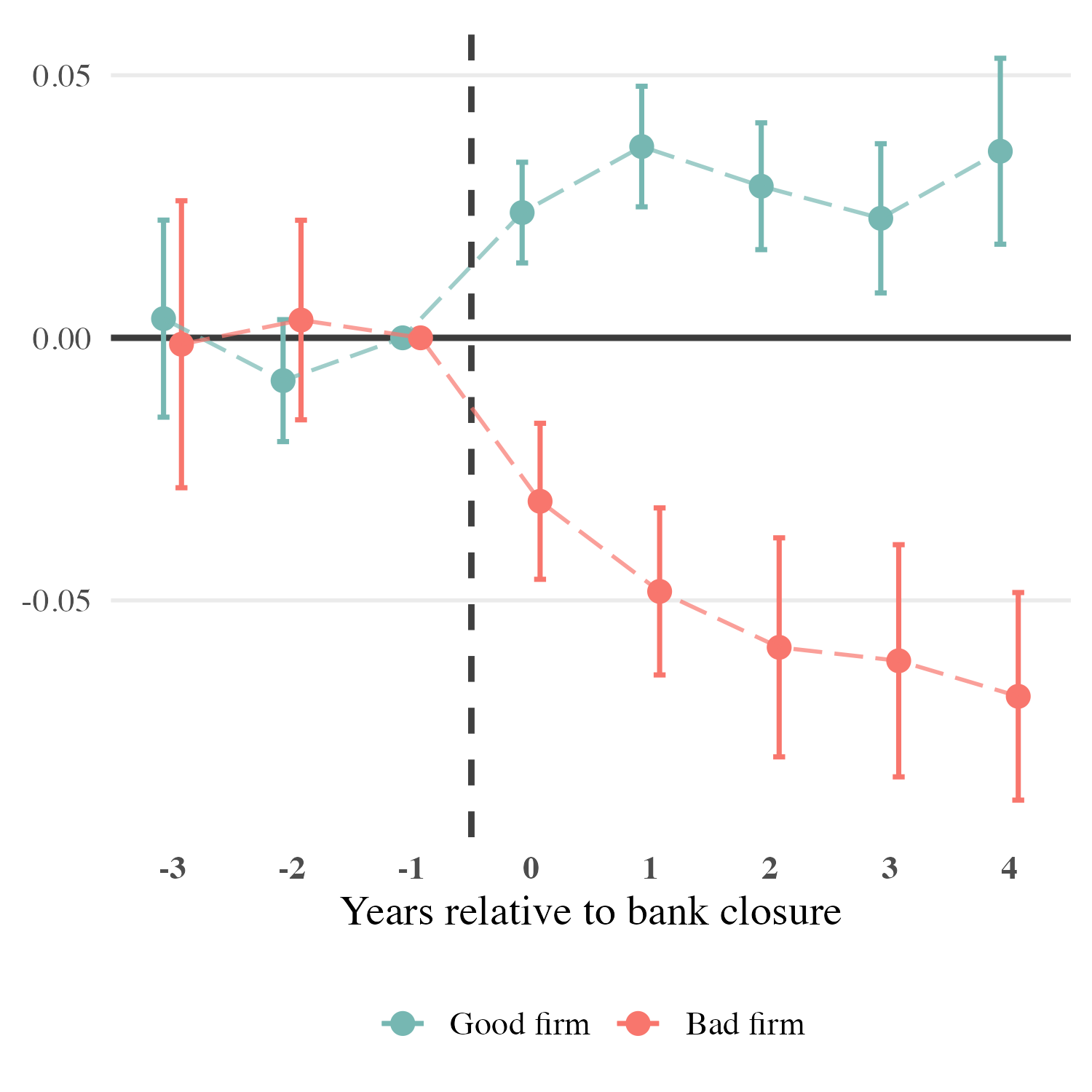

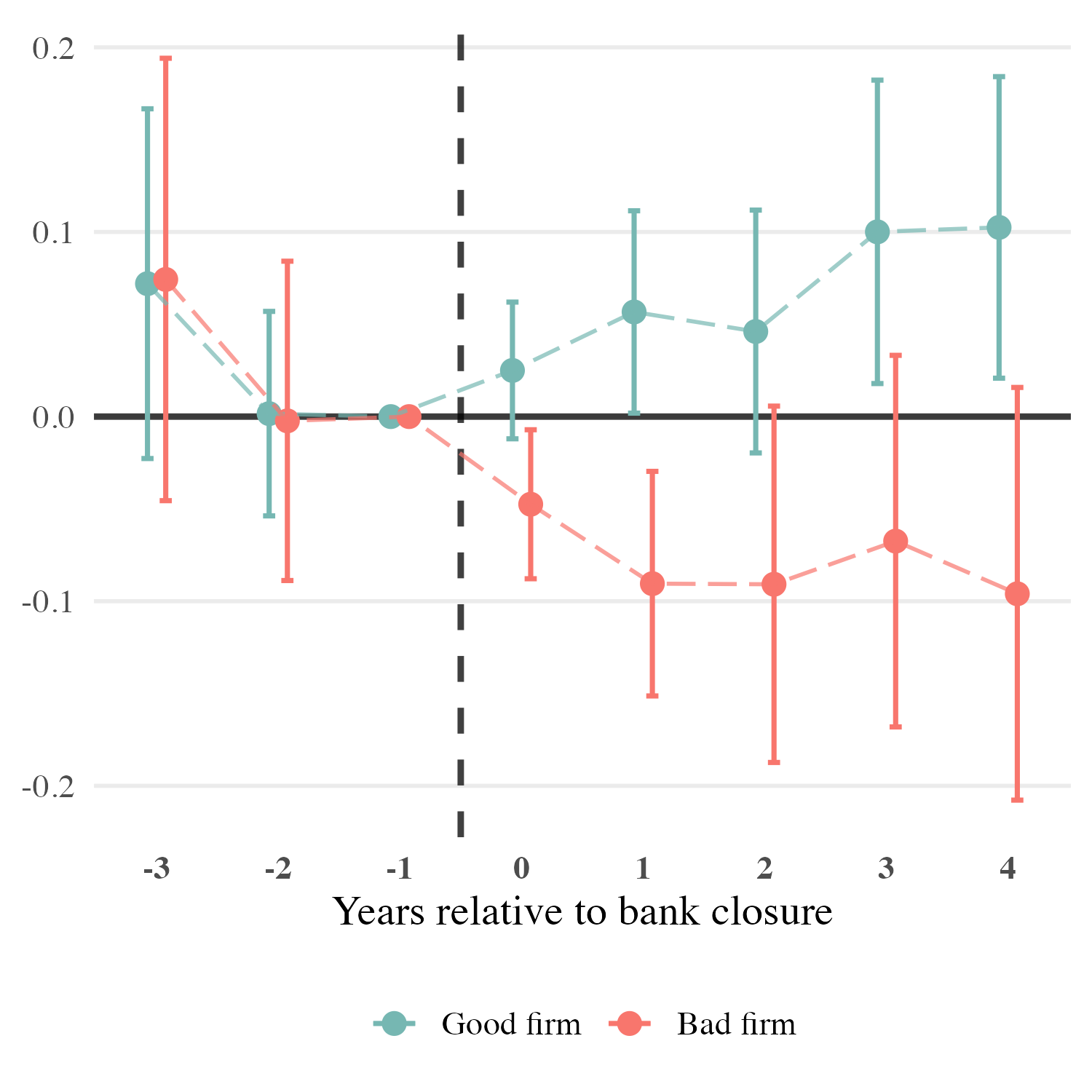

Figure 1. This figure presents the results of the firm-level event-study analysis by depicting the values of event-time coefficients \( \beta_{\tau} \) (green) and \( \gamma_{\tau} \) (red) of the event-study regression below:

\[ \begin{aligned} Y_{f,t} =\;& \alpha_f + \gamma_{s,t} + \lambda_{r,t} \\ &+ \sum_{\tau \neq -1} \beta_{\tau}\, \mathrm{BankClosure}_{m,t} \times \mathbf{1}\{t=\tau\}_{m,t} \\ &+ \sum_{\tau \neq -1} \gamma_{\tau}\, \mathrm{BankClosure}_{m,t} \times \mathbf{1}\{t=\tau\}_{m,t} \times \mathrm{BadFirm}_{f,t} \\ &+ \mathbf{X}_{f,t-1}\mathbf{\Theta}' + \varepsilon_{f,t} \end{aligned} \] where the former and the latter capturing respectively: the direct response of 'good' firms to the fact of bank closure in municipality of its location at time \( t \), as well as the differencial response of the 'bad' firms. Firm is labelled 'bad' if it is classified as high-risk according to Zmijewski bankruptcy prediction model.

\[ \begin{aligned} Y_{f,t} =\;& \alpha_f + \gamma_{s,t} + \lambda_{r,t} \\ &+ \sum_{\tau \neq -1} \beta_{\tau}\, \mathrm{BankClosure}_{m,t} \times \mathbf{1}\{t=\tau\}_{m,t} \\ &+ \sum_{\tau \neq -1} \gamma_{\tau}\, \mathrm{BankClosure}_{m,t} \times \mathbf{1}\{t=\tau\}_{m,t} \times \mathrm{BadFirm}_{f,t} \\ &+ \mathbf{X}_{f,t-1}\mathbf{\Theta}' + \varepsilon_{f,t} \end{aligned} \] where the former and the latter capturing respectively: the direct response of 'good' firms to the fact of bank closure in municipality of its location at time \( t \), as well as the differencial response of the 'bad' firms. Firm is labelled 'bad' if it is classified as high-risk according to Zmijewski bankruptcy prediction model.

Figure 2. Number of bank branches in Russia, 2008-2024

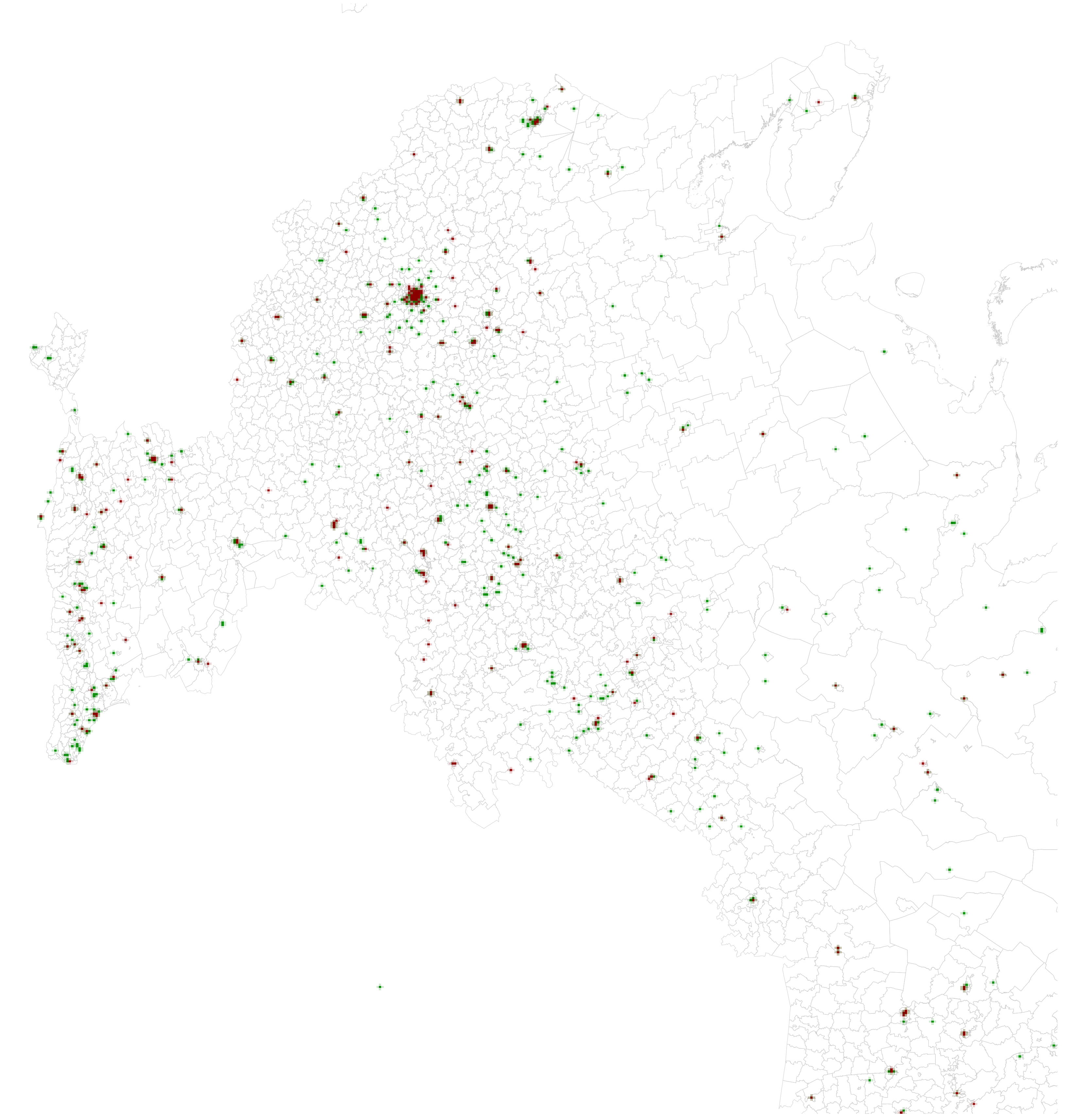

Figure 3. The map illustrates geographical distribution of Russian banking system based on geolocated addresses of all Russian banks' headquarters and branches as of Q1 2013. Red and green dots represent bank headquarters and branches, respectively.

Invisible Lines: How Banks Use Firm Networks to Blunt Supervisory Tightening

› abstract

Abstract: This paper proposes a novel approach to measuring banking fraud, which we apply in a setting characterized by a sharp decline in regulatory forbearance, where the central bank shut down roughly two-thirds of Russian banks for fraudulent activity. We develop an empirical model of the supervisory decision rule governing unscheduled on-site inspections of suspect banks. Using predictions from the estimated rule, we define a treatment group of likely-to-be-inspected banks and implement de Chaisemartin and D’Haultfoeuille (2017) difference-in-differences regressions to estimate the effects of regulatory tightening. The baseline estimates show a substantial decline in treated banks’ asset size; however, this masks sharp heterogeneity. Using unique firm-ownership registry data, we measure each bank’s ego-network complexity and find that ownership networks are pivotal for adjustment to tighter supervision: weakly connected banks contract, cutting assets and equity, while well-connected banks expand their balance sheets and shift from consumer toward corporate lending.

Figure 1. The figure depicts the estimates from the de Chaisemartin and D’Haultfoeuille (2017) type of difference-in-difference analysis where treatment event is defined as getting susceptible to the central bank and response is differenciated by bank ownership network type. Banks are labelled as having 'rich' network if their network's out-degree network metric (number of outgoing relationship edges) is int the top 10% of the distribution and labelled as 'poor' otherwise. The analysis includes only ’switchers-in’ banks (in de Chaisemartin and D’Haultfoeuille (2017) notation) in the treatment group. Bank profile × quarter fixed effects are included to allow for different dynamics for banks with different business models, which we capture by Bank profile bins

being constructed as a combination of four dummies for: bank size and share of firm loans to assets (below or above median), and state and foreign bank dummies.

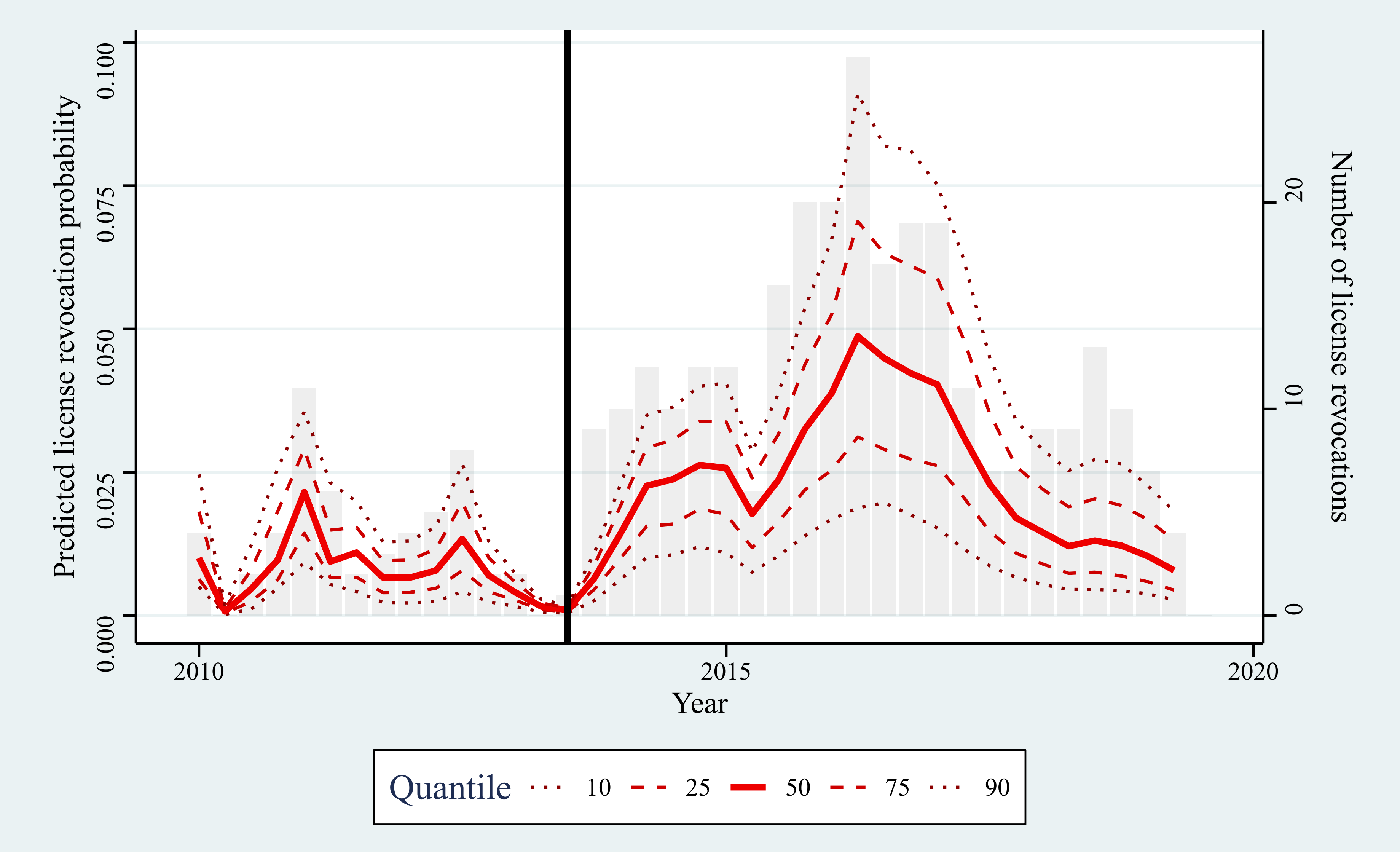

Figure 2. The figure illustrates the dynamics of the predicted probabilites of fraud detection in the Russian banking system during the 2010s. Red lines represent the correspnding quantiles of the predicted probabilities distribution, where each probability value is a result of estimated logistic regression over the 2-year rolling window. Grey bars represent the number of close banks in a given quarter. Vertical black line delineates the Q2 of 2013 - the date of new central bank head appointment.

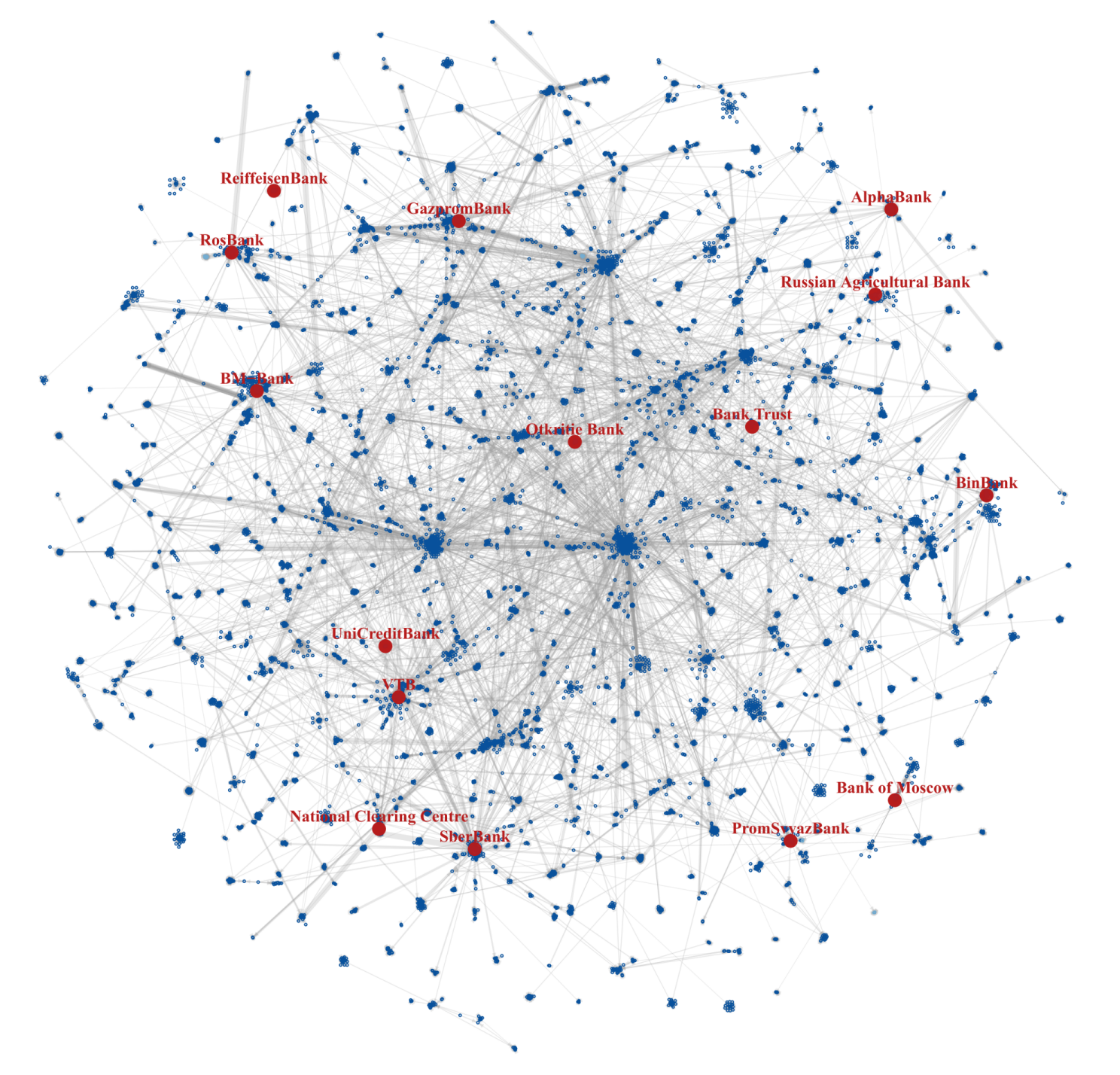

Figure 3. The figure illustrates ownership networks of the 15 largest Russian banks one quarter before Nabiullina appointment (in 2013-Q2) by showing each bank’s ego network up to the fourth degree depth (where first degree is represented by direct owners or firms owned by bank b, second - by owners and firms owned by the first degree counterparties and so forth). Banks are illustrated as red dots with associated red labels. Blue dots represent all other firms in the network. Ownership links are plotted as gray arrows.

Work in Progress

Political Lending Along the 'Freedom Ladder'

Single authored

› abstract

Abstract: What politicians do to stay in power? Existing work shows that incumbents maximize their re-election chances through cycles of fiscal spending or lending by state banks. Yet either of the two instruments has been studied in isolation and exclusively in democratic setting, while recent evidence documents that more countries are drifting toward authoritarian rule. This paper aims to generalize existing evidence by tracing evolution of fiscal and lending cycles along a country’s path down the ‘freedom ladder’. I further test whether political use of state banks goes beyond previously documented rent extraction and tactical redistribution but also serves to maintain political control, by using credit to offset center–periphery frictions and to respond quickly to episodes of social unrest. The analysis also requires bringing protests, repression, and propaganda into the empirical framework, which has not been done yet due to severe scarcity of such data. I aim to fill this gap by drawing on an arguably most comprehensive hand-collected single-country dataset, providing insight into two decades of political life in Russia.

The Political Economy of Subsidy Allocation: the Role of Banks

› abstract

Abstract: This paper explores how partisan (mis)alignment shapes the outcomes of industrial subsidy policy within a federal democracy. We document a case where alignment appears to grease the wheels of policy implementation by facilitating the bottom-up information transfer about subsidy applicants through aligned local state banks. Drawing on granular subsidy data and hand-collected county-level election results spanning more than two decades (2000–2019), we find that counties aligned with their state governments receive substantially more subsidies, while these transfers translate into higher investment and employment, effectively serving the program’s intended purpose. The effects are more pronounced in counties with higher per capita lending by local state banks while being not related to lending by otherwise comparable control group of private cooperative banks.

Healing Markets: Repression, Victimization and Market Reforms

› abstract

Abstract: This paper investigates whether the development of market institutions can mitigate the long-term economic "scars" left by historical political repressions. While a body of literature documents the persistence of historical effects in economic behavior, few studies explore the conditions under which these effects can be reversed. We hypothesize that marketization facilitates a critical transition from relational exchange—dependent on personal reputation and family background—to impersonal exchange governed by formal rules, credit scores, and transparent contracts. In doing so, market-oriented reforms may render the "victimization" of previous generations irrelevant to modern economic outcomes.

Utilizing a novel, high-resolution dataset, we measure municipality-level repression intensity using geocoded arrest addresses from the Stalinist era in Russia. We match this with a newly constructed, registry-based Marketization Index covering over 2,600 municipalities, which captures firm dynamism (entry-to-exit rates), financial access, privatization, and the efficiency of contract enforcement and insolvency proceedings. We then examine the impact of historical repression on contemporary personal default rates and debt burdens.

We aim to test whether regions with higher historical repression intensity exhibit higher rates of personal insolvency today, and crucially, whether the presence of robust market institutions attenuates this relationship. This study provides some of the first empirical evidence on the reversibility of historical scars, suggesting that competitive markets can "punish" the persistence of discrimination and victimization by prioritizing institutional merit over historical background.